In the finance world, the borrowing system took a long time, and every so often, it turned into unfairness. Due to gradual processes and bad discretionary decisions, people could not easily access credit. This has made it difficult for many people to get the assistance they want. So, wise people presented actual loans. It’s like an incredibly clever system that uses laptop trickery to make it easier and extra handy for everyone to get a loan. But because it matures, it has a few troubles that want to be constant.

Automated lending: Simplifying loan approvals

Automated lending has changed how loans are approved. This includes using a PC chart to assess and regularly identify individuals or entities used for financial assistance. It sounds like a great exchange about how costs work! Let’s dig in and find out how this attractive form of lending has made a massive difference in how banking and manufacturing help people.

Why Automation in Lending Can Do More Than You Think

Automated lending isn’t just a faster way to get a loan; it’s changing how borrowing works for everyone. In the past, getting a loan could be slow and difficult, especially if you didn’t have a perfect credit history or a traditional job. But automation is making things easier and fairer.

Here’s how:

- It looks at more than just your credit score – It can check your payment history, bills, or even other data to help decide if you qualify for a loan.

- It removes human bias – Since a computer makes the decision, it’s based on facts, not feelings or assumptions.

- It’s super quick – You can get approved in minutes instead of waiting days or weeks.

- It helps more people gain access. People who were previously excluded can now access loans because the system considers more than just the basics.

So, automation in lending isn’t just about speed. It’s about giving more people a fair chance to get the money they need, when they need it.

Automated Lending Process

Automated Lending Process uses PC algorithms, algorithms and other technologies to make mortgage decisions without direct human involvement. Credit reports and benefits information are examined to quickly decide whether or not a person qualifies for a loan under certain circumstances. These actions aim to greenen the mortgage process by considering technologies for expedited credit assessment.

Types of Automated Lending Systems

Machine Learning Framework

One of the main functions of automated loans is that the system works to acquire knowledge, read ancient statistics and determine the likelihood of mortgage acceptance or rejection. By learning strategies from large datasets, those algorithms provide predictive algorithms that greatly simplify the method selection process.

Artificial Intelligence (AI) Systems

In research, artificial intelligence systems go into past historical records. They use much information, not just beyond credit ratings, to make informed decisions. This comprehensive approach allows for more specific testing, making rent approval more accurate.

Advantages of Automated Lending

Here are a number of the benefits you may get with the assistance of Automated Lending:

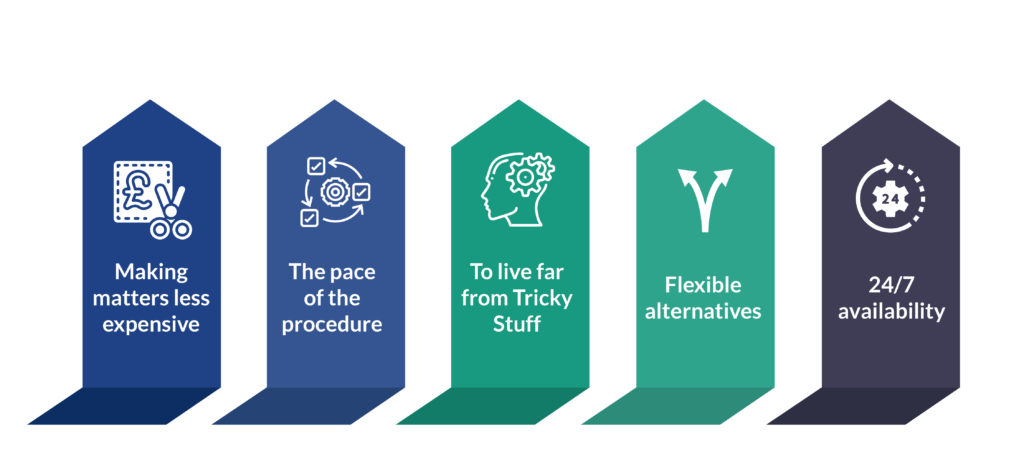

- Making matters less expensive – Automated lending helps folks with low or medium incomes by giving them access to loans they might not usually get. That way, extra people can come up with the money to pay for their goals, including an automobile or house.

- The pace of the procedure – Renting a loan can take a long term, right? But with automated lending, it’s quicker. The computer speeds up the approval system, so you don’t continually have to wait to find out if you’ll get that loan.

- To live far from Tricky Stuff – It can be a trouble for fraudsters seeking to scam people out of cash. But those clever PC systems can stumble on them and prevent loans. That saves you money!

- Flexible alternatives – Passive loans provide greater alternatives depending on your wants. These plugins can speed up your search via huge statistics, making it less complicated than allowing you to provide the right mortgage you’re looking for.

- 24/7 availability – Imagine being able to apply for a mortgage at any time, day or night time! The digital loan provider works around the clock, no matter what business office hours are, allowing you to apply whenever mileage is handy.

Disadvantages of Automated Lending

Despite its efficiency and clever design, Automated Lending faces inherent limitations. So here are several problems with self-credit loans.

- At least informal communication – Automation lacks the human touch. Sometimes, you may need to talk to someone about your finances, or you may need someone to understand your unique situation. Computers can’t do that.

- Complete reliance on records – These programs are heavily information-based. Having hiccups with facts or missing data can impact your mortgage prospects, and the gadget won’t keep any new information in mind beyond what it’s programmed to see.

- Possible errors – Computers are smart and still not the best. There can be errors in algorithms or misinterpretation of statistics, resulting in an unfair judgment of your credit score.

- Limited references – Automated structures work entirely on patterns and algorithms. You’ve told a bigger picture of your financial situation or motivation behind some data, which a viewer can better understand.

- Difficult speeches – If the system denies your loan, it may be difficult to determine why. Unlike someone who can explain a decision, a laptop doesn’t prevent one from making good judgments or feeling rejected.

Enhancements and Future of Automated Lending

The success of automated lending lies in its ability to integrate human knowledge into the process. The accuracy of mortgage approvals can be raised by combining automated methods with insightful assessments provided by human inspectors. Additionally, ongoing data analysis and process improvements promise a more robust future for automated lending.

Regulatory Framework for Automated Lending

Automated lending, also known as automatic clearing and compromise (ACS), is using age to handle financial transactions that people don’t want to get involved in. It’s like a groovy tech wizard backstage, making banking smooth the global picture. This form of automated lending has been a hit in the banking industry but is subject to far greater regulatory oversight. There are two main types of automated lending:

- Automated Credit Scoring: This automatic credit scoring is like a discreet device that tests consumers’ confidence regarding credit scores. One uses fancy math to determine if one is eligible for a scholarship.

- Automated underwriting: Here, the machine uses special algorithms to learn about loan profitability and determine if taking out a loan is a great idea.

Then, regarding regulations and standards, there is a big one called the Electronic Funds Transfer Act (EFTA) of 1978. This regulation is concerned with how funds move between banks. The judge ensures everything goes smoothly as the computers process the bills.

Regulators, including the Bank of England and the Financial Conduct Authority (FCA), have raised concerns about the real lending practices inside the UK industry. For instance, the Bank of England highlighted the dangers of automatic lending merchandise in 2013. However, the FCA issued guidance in 2015 on the use of digital systems for lending choices

Thus, as generations change how money circulates, those guidelines and signals help keep lending fair, safe, and internationally reliable. They make sure that when teammates do the heavy lifting, it is executed miles away as authentic or even for everyone involved.

Why Automated Payments Matter for Lenders

Obtaining a loan is one thing, but repaying it on time is just as important. That’s where automated payments come in. These are payments that occur automatically, without requiring any action on your part.

Here’s why they matter:

- They ensure that payments are made on time. When payments are automatic, people are less likely to forget or miss them.

- They save time and effort – Lenders don’t have to send reminders or chase payments.

- They make things easier for borrowers – no more worrying about payment dates; just set it up and relax.

- They help spot problems early – If a payment fails, the system can send an alert right away.

For lenders, automated payments help everything run smoothly. For borrowers, it’s one less thing to worry about. It’s a win-win.

FAQ

What are the 5 Cs of lending?

The 5 Cs are Character, Capacity, Capital, Collateral, and Conditions. These help lenders decide if you’re likely to repay a loan by looking at your credit history, income, savings, assets, and the purpose of the loan.

What is AI lending?

AI lending refers to the use of artificial intelligence, specifically innovative computer programs, to determine an individual’s eligibility for a loan. It analyses data such as credit history, income, and spending patterns to make quick, fair loan decisions.

What is automated securities lending?

This is when computers facilitate the lending of stocks or bonds (called securities) from one party to another. Investors and banks often use it to earn extra money when they are not using those securities.

How do banks make lending decisions?

Banks look at your credit score, income, debts, and sometimes the 5 Cs of credit. Today, many banks also utilise automation and software to expedite the process and make more informed decisions.

Do banks create money through lending?

Yes, in a way. When banks give out loans, they don’t hand over existing money—they create new money that gets added to the economy. This is called credit creation.

What is the danger of putting up collateral for a loan?

If you don’t repay the loan, you could lose whatever you offered as collateral, like your car or home. It helps the lender feel more secure, but it’s risky for the borrower if things go wrong.How does auto lending work?

Auto lending refers to the use of software to automate the approval, management, or repayment of loans. It checks your details, makes a decision quickly, and can also set up payments without requiring manual intervention.

How DataGardener can help you

DataGardener’s APIs, such as Company, Finance, Land Registry, Related Companies and Company Document APIs, offer essential facts for automatic lending. Integrating those APIs improves borrowing by using the agency’s detailed insights, financial information, and asset facts and raising critical documents. These rich records improve hazard evaluation, compliance, and informed lending selections, making the automated lending procedure more efficient and accurate.

Conclusion

Automated settlement systems are gaining momentum in the financial sector, speeding up loan approvals and increasing productivity. However, relying entirely on historical statistics or records can sometimes lead to wrong conclusions. The combination of technology and human insights is a promising approach to the destiny of automated lending.