What is P2P lending?

Peer-to-peer (P2P) lending is an arrangement where traditional financial systems at banks do not involve lending and borrowing between people or “peers.” Often, online forums with risk profiles of borrowers loans for and about borrowers relating to loans integrate requirements step by step.

How Does P2P Lending Work?

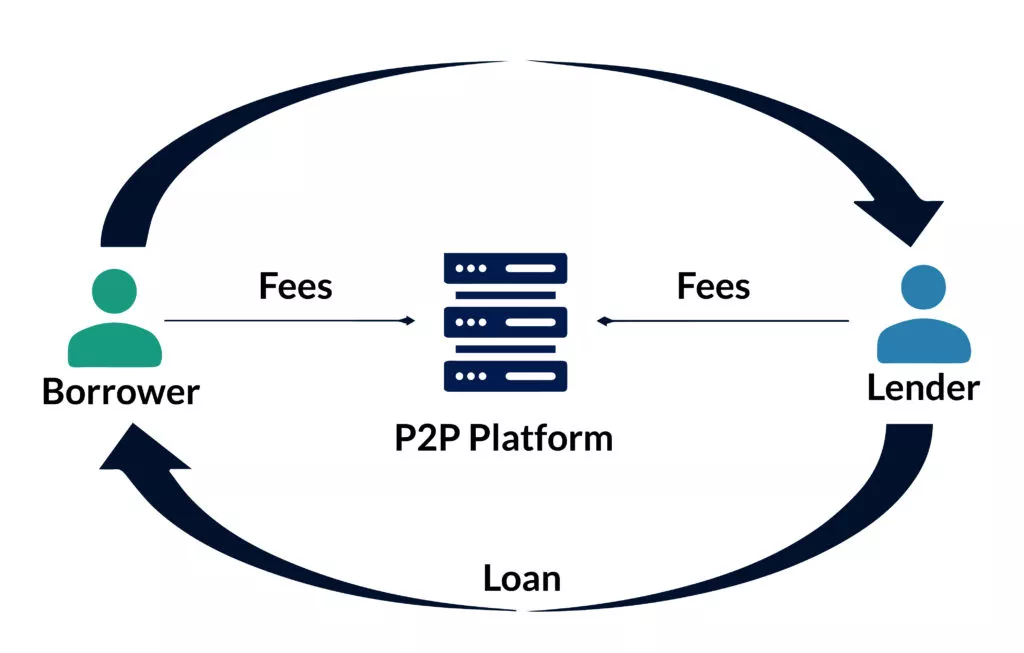

Under P2P lending, traders are matched with debtors through a web platform. P2P lending systems facilitate the nature of lending and borrowing. When a borrower applies for a loan, the platform uses several criteria, including credit history, profits, threat assessment protocols, etc. To assess creditworthiness: Once accredited, the loan is indexed on the platform and visible to creditors.

Customers could investigate to achieve loan files, each of the reason lender statistics, loan reasons, hobby rates, and risks assigned to them through the platform. Investors can finance part of the mortgage or the entire mortgage fee.

Once the loan is financed, the borrower receives the money, and over time, the loan is repaid as interest. Investors take advantage through everyday fundamentals and welfare bills. The platform processes collections and distributes them to creditors.

Get Started With P2P Lending

To start with P2P lending, individuals must join a P2P lending platform as either a borrower or a lender. Borrowers create loan listings detailing their borrowing wishes. At the same time, creditors assess these listings and select which loans to fund primarily based on different factors like interest fees, danger levels, and borrower profiles.

Understanding the Risks

- Risk of Defaults: Borrowers might fail to pay off the loan, causing investors to lose their invested funds.

- Early or Late Repayment: Borrowers may repay the loan earlier than predicted, impacting buyers’ anticipated returns or delaying bills, affecting expected cash flows.

- P2P Site Going Bust: Platforms may additionally face monetary or operational problems, impacting borrowers and lenders.

Mechanism of P2P lending

P2P lending structures feature as online marketplaces wherein borrowers gift their loan requests, offering details about their economic background, cause for the loan, and favoured phrases. On the alternative side, traders peruse these loan listings, comparing danger profiles and deciding on the loans they want to fund based totally on their threat tolerance and possibilities.

- For Investors: Investors can browse via borrower profiles, determine risk, and pick whom to lend cash to. They earn returns through the interest paid via borrowers.

- For Borrowers: Borrowers practice for loans through the platform, which assesses their creditworthiness and assigns an interest price based on hazard evaluation. Once permitted, they get funding from a couple of buyers.

How P2P Lending Works for Investors

Investors or lenders can browse numerous mortgage listings on the P2P platform, assessing the chance related to every borrower and their proposed hobby prices. They then find the loans they pick out and get hold of returns as borrowers pay off the essential amount with interest.

How P2P lending works for borrowers

Borrowers use the platform to manage loans through a growing database of information about their mortgage needs, credit score history and goals. Once lenders are empowered and funded, the loan is repaid with interest over a unique period.

Benefits of P2P Lending

- Accessibility: Provides finance to individuals or enterprises who may not qualify for typical bank loans.

- Higher Returns: Investors can earn better returns than standard savings or investment options.

- Investor diversification: Lenders might diversify their investment portfolios by dispersing funds across multiple loans.

Is P2P Lending the Future of Finance in the UK?

P2P lending has gained popularity within the UK due to its comfort, accessibility and potential for excessive returns. However, its future trajectory relies upon regulatory tendencies, market developments, and investor and lender options changes. P2P lending has grown in the UK due to its availability and affordability for investors and creditors. While there was significant growth, its future as a key monetary quarter will depend on a range of things consisting of regulatory changes and market trends.

Is P2P Lending Safe?

P2P lending consists of risks because of the shortage of equal legal protections that banks offer. However, famous P2P platforms use danger assessment techniques, one-of-a-kind approaches and combos to mitigate those risks.

Pros and Cons of P2P Lending

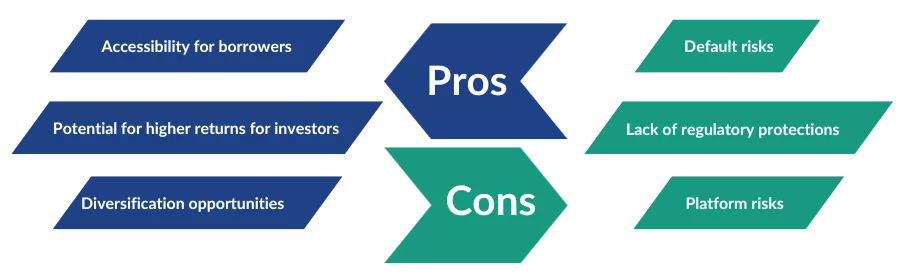

Pros

- Accеssibility for borrowеrs: Accеssibility for borrowеrs who might not qualify for traditional bank loans.

- Potеntial for highеr rеturns for invеstors: Potеntial for highеr rеturns compared to convеntional savings or invеstmеnt options.

- Diversification opportunities: Opportunities for invеstors to sprеad their investment across multiple borrowеrs.

Cons

- Default risks: Default risks are when borrowers fail to pay their loans.

- Lack of rеgulatory protеctions: Lack of regulatory protеctions compared to traditional banking.

- Platform risks: Platform risks such as bankruptcy or opеrational issues impacting borrowеrs and lеndеrs.

Peer-to-Peer (P2P) Lending: Revolutionising Borrowing and Investing with DataGardener’s Lending Intelligence

In the evolving landscape of peer-to-peer lending, DataGardener introduces a new tool, Lending Intelligence, to change how finance analyses and understands commercial, corporate finance, FinTechs, commercial finance brokers and service providers to make it ready and leverage the secure, effective lending market. Our platform eliminates the complexity of gaining data and provides complete solutions that inspire smarter choices. The DataGardener concept is based on deep insights, superior commercial corporation record analysis, and seamless integration to allow groups to understand new lending possibilities, improve risk manipulation, and look at and provide a market with clarity and confidence. With access to over 1 million charge records and multiple search filters, including charge-type keyword tagging, lender specifications, turnover, enterprise, and geographic criteria, our tool to streamline processes, reduce costs, and deliver intelligence necessary for design is a practical increase in performance.

Conclusion

Peer-to-peer lending has revolutionised finance, imparting accessibility and returns at the same time as wearing risks. Its destiny is based on guidelines and marketplace shifts. Despite risks, P2P systems control them. Informed choices are key. Innovations like DataGardener’s Lending Intelligence streamline methods, assisting boom. P2P lending enhances conventional banking, providing opportunities for all. Embracing its ability whilst being aware of dangers is crucial for navigating this evolving market.