With so many options, choosing a mortgage lender can feel overwhelming, especially when considering the various types of mortgage lenders, such as retail lenders, direct lenders, and agents. Every lender does things a little differently, and that can be difficult. But understanding the difference allows you to make superior choices.

Finding the perfect lender isn’t just about the type of loan they have; it’s about saving money, time, and stress. That’s why it’s important to take some time and look at specific lenders. There are various types of retail lenders, direct lenders and agents. Sometimes, they do comparable jobs, which can be hard to tell.

Mortgage Lender

The mortgage lender is the main hyperlink between prospective homeowners and prospective financial buyers. These institutions or banks provide financial assistance to set up vocabularies, interest profiles, and reward systems through family loans. They assess applicants’ qualifications, guide them through the loan process, and offer mortgage options based entirely on their preferences.

Key Points about Mortgage Lenders

Here are some important points about mortgage lenders:

- Many lenders consider the fees for that offering.

- Retail lenders offer instant mortgages.

- Direct lenders make their loans using their capital or sources of income.

- Wholesale lenders, including banks or financial institutions, do not interact with consumers without delay but originate, repay, and hold a loan once.

- Correspondent lenders work because the original mortgage lender is negotiable.

- Warehouse lenders help other borrowers pay their bills by providing quick financing.

The Main Types of Mortgage Lenders

Here are some main types of mortgage lenders:

Mortgage bankers

Big banks such as Barclays and NatWest are key players in the UK home mortgage enterprise, online lenders and Lloyds Bank. They use behavioural information and partnerships with financial institutions to offer loan options. From conventional fashionable loans to specialised applications that include senior rehabilitation, those lenders, large or small, meet requirements while adhering to enterprise rules.

Direct Lenders

Direct creditors offer one-time loans to debtors with credit-rating unions and mutual funds. They specialise in mortgages and offer many options, from conventional to jumbo loans. Unlike retail creditors, direct lenders face the whole mortgage method in-house, with external intermediaries. With an extensive online presence, they offer lenders faster mortgage processing and greater personal taste, which has put off the need for third parties.

Portfolio lenders

Portfolio lenders, including community banks, finance the mortgage with their own money and preserve it at home instead of selling it. This flexibility allows the advent of a private credit scoring device, which additionally caters to folks who want larger loans or are out of labour and opt for traditional lenders. Lenders can be more forgiving and take longer sentences, but due to the fact that those loans are risky, they regularly encompass accurate credit and leisure statistics. While preliminary offers can be made for flexibility, lenders ought to weigh the fees in opposition to the benefits of the selected mortgage.

Wholesale lenders

Wholesale lenders work behind the scenes, offering loans with merchants, banks, or credit score unions. Although their names appear on loan files, they’re not directly visible to debtors. Loan terms and budgets are set up, but debtors interact with intermediaries who take care of administration and documentation. Although important, they do not appear to have lots of utility for job seekers handling a lending intermediary or economic organisation.

Correspondent Lenders

In the UK loan market, correspondent lenders originate, underwrite, and fund loans, often selling them to larger lenders or brokers. They drive up the price, thereby turning loans, offering these miles, and processing the loans the customer was responsible for doing. If the investor rejects the loan, the lender unveils a new buyer or retains the loan. While the correspondent can work with lenders to provide expedited policies and procedures, lenders must rely on the preparation and additional financial information they can provide their business to help the manual borrowers through the loan process.

Retail lenders

UK retail creditors, running with banks, credit unions, and creditors, serve customers directly with some monetary merchandise consisting of institutional loans, personal loans, and automobile loans. They streamline the lending technique, simplifying actual estate transactions. These lenders provide financing and storefront alternatives, assisting customers in selecting the proper mortgage terms.

Warehouse Lenders

Warehouse lenders offer short-term financing to various lenders, including small banks or media lenders, so they can make their loans. Let those lenders tell consumers this instead of using the bonds as collateral until the mortgage is purchased on the secondary market. Once the loan is sold, the proceeds pay the warehouse lender’s credit score facility. This software allows microlenders to raise prices and keep the housing market afloat.

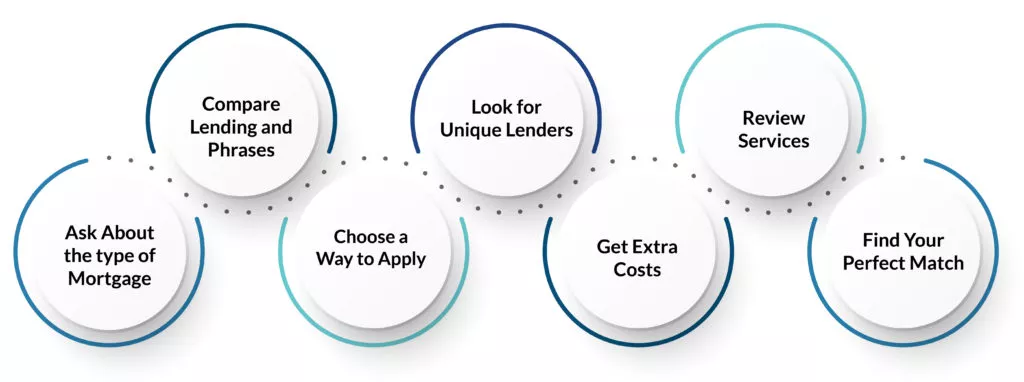

How to Choose the Right Lender

If you’re new to the home business, finding a lender who can be precise and firm and guide you through the process is wise. Look for lenders considering refinancing that are recognised for their knowledge of refinancing options. If you are a veteran or have a low credit score, consider finding a lender focusing on special government-subsidised loans that fit your situation. These lenders can offer flexible options and superior guidance based primarily on your specific needs and terms.

- Ask about the type of mortgage: Ask approximately what type of mortgage they have.

- Compare lending and phrases: Check lending and credit standards.

- Choose a way to apply: Apply online or in person, whichever suits you best.

- Look for unique lenders: Don’t stick with one; research one-of-a-kind lenders.

- Get extra costs: Getting charges from one-of-a-kind creditors can save you money.

- Review services: Look at what each lender gives, their charges, and their customer service.

- Find Your Perfect Match: This is set up to locate the proper lender for your dream home!

How DataGardener can help you

DataGardener is your go-to source for all things related to mortgage lenders. If you’re in the lending industry or connected to it, you will find comprehensive information and valuable insights about every company or individual. DataGardener has you included in its vast database for anyone seeking insights about UK lenders. It includes the essential active mortgages in the UK marketplace, offering a one-stop store for crucial statistics. Whether looking for lenders unique to your mortgage desires or trying to grow your business, DataGardener has all of it.

Conclusion

In conclusion, understanding the strategies and services of lenders can put you in the right position. Whether it’s clear descriptions, refinancing expertise, or basic loans, each lender offers unique benefits. You can find the perfect match by identifying your options, analysing the different aspects, and deciding on an appropriate decision-making strategy.

Leave a Reply

You must be logged in to post a comment.