If you owe money to a creditor and fail to keep up with repayments, they might take legal action against you. When all other attempts to recover the debt fail, a creditor can apply for a County Court Judgment (CCJ) to be issued against you.

Here’s a comprehensive guide to understanding CCJs, their impact, and how to deal with them.

What is a County Court Judgment (CCJ)?

A County Court Judgment (CCJ) is a court order that compels you to repay a debt. It means the court has determined that you owe money to a creditor. This step is usually taken as a last resort after the creditor has tried other means to recover the debt.

How do you know if you have a CCJ?

You will receive a County Claim Form before a CCJ is issued. This form includes details of the debt, the amount owed, and instructions on how and when to pay it. If you do not respond to this notice within 14 days, a CCJ will be filed against you.

Checking for County Court Judgments

You can check whether you have a CCJ or not by:

- Requesting your credit report from a credit reference agency.

- Searching the Registry Trust online, which holds records of all CCJs.

How a CCJ Affects Your Credit Score

A CCJ will be recorded on your credit file, severely affecting your credit score for six years. This makes obtaining credit, such as loans or mortgages, difficult during this period. The impact might lessen over time if you manage your credit responsibly.

Responding to a CCJ Claim

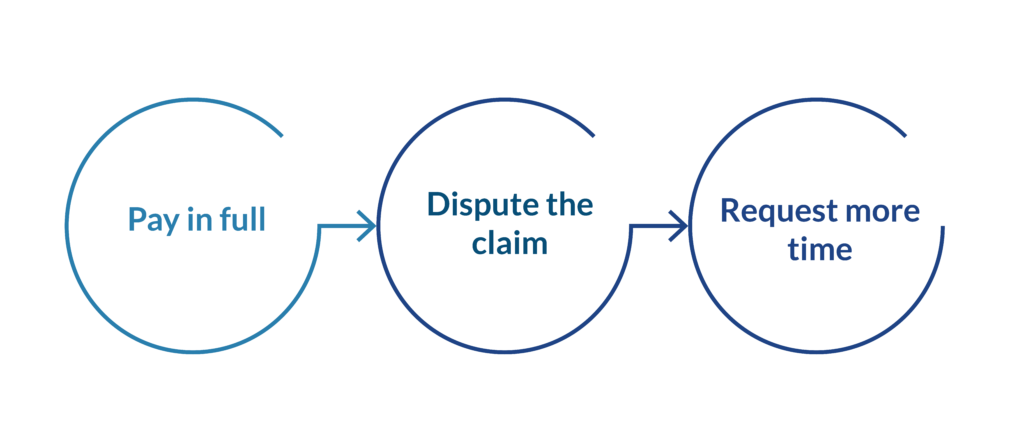

When you receive a CCJ claim form, you must respond by the deadline to avoid further action. Here are your options:

- Pay in full: If you pay the debt in full within 28 days, the CCJ will not appear on your credit record.

- Dispute the claim: If you think you don’t have the debt or have already paid it off, you can defend the claim.

- Request more time: You can request a 14-day extension by sending a service form to the court.

Consequences of Ignoring CCJ

There is no way to ignore and remove the CCJ report. The court may enforce the debt in a variety of ways:

- Bailiffs: Designated court officers can go to your home to collect money or seize items to sell and pay debts.

- Attachment of Earnings Order: You can deduct money directly from your salary.

- Charge order: A charge can be placed on your property, meaning you could lose if the debt is unpaid.

County Court Judgments Removal or Satisfaction

After six years, the CCJ is automatically removed from your credit file. You can apply for immediate discharge if you pay the entire debt within one month of the judgment. If you say later, your report can mark it as ‘satisfactory’.

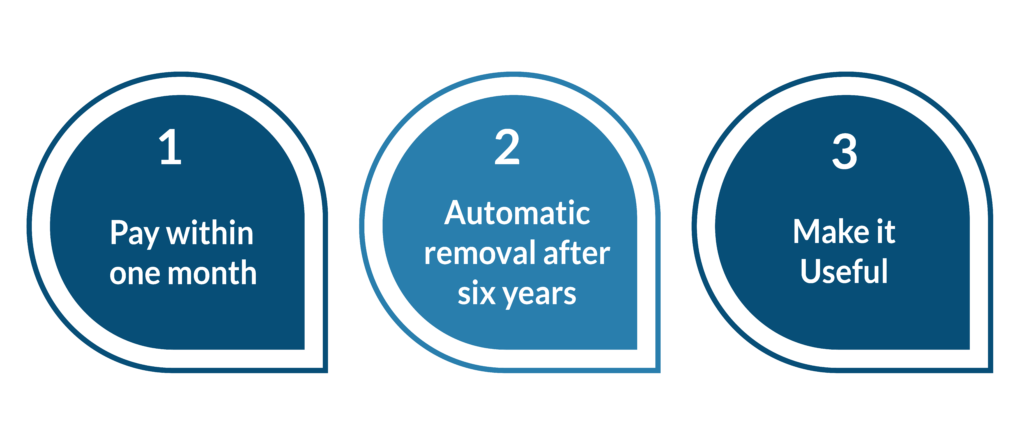

Three Ways to Remove CCJ from Your Credit Report

- Pay within one month – If the CCJ is paid in full within one month of the decision date, the court will permanently remove the CCJ from your credit report. This is the best option if you can afford a loan and arrange quick payments.

- Automatic removal after six years – The CCJ will be automatically removed from your credit report after six years even if the loan is not repaid. However, in the meantime, the claimant can still control the unpaid debt through a lien or wage garnishment.

- Make it useful – If you think it was issued in error or you did not receive a receipt, you can apply to have the CCJ set aside. To do this, you must complete form N244 and file it with the court, explaining why. If successful, the court will remove the CCJ from your record.

Avoiding County Court Judgments

To avoid a CCJ, contact your lender when you realise your default. Many lenders prefer to work out a payment plan rather than go to court. The key is to be proactive and honest about your situation.

Application for Credit at CCJ

Having a CCJ makes it harder to get promoted, but not impossible. Lenders will consider factors such as:

- How up-to-date is the CCJ?

- Is CCJ marked as ‘satisfactory’?

- The money you owe.

If you are applying for a mortgage or loan with a CCJ on your record, consult a financial advisor for personalised advice.

FAQs

How long does a CCJ stay on your credit report?

Regardless of whether the loan is paid or not, the district court judgment will stay on your credit report for six years from the date of the judgment. If you pay the full amount within a month of the decision, you can request that it be removed from your credit report altogether. Otherwise, once the CCJ is paid, it will be marked as ‘satisfactory’ but remain on record for six years.

Can the lender see my CCJ after six years?

After six years of removing a CCJ from your credit report, lenders can no longer detect it through conventional credit checks. However, if the debt is still unpaid, the lender may have other options to consolidate the debt. You must pay any outstanding debts to avoid further legal action.

How to check for CCJs?

Public records and paid online services like DataGardener can provide information about the company, including details on any County Court Judgments (CCJs) filed against it. This includes the court order, the amount of debt, and when the CCJs were issued.

DataGardener also offers a monitoring service to keep you updated on any changes to a company’s CCJ status, which can help assess its financial history and creditworthiness. This information can be useful when working with new or existing clients.

Final Thoughts

Dealing with CCJs can be challenging, but understanding how they work and how to handle them can help minimise their impact on your financial health. It’s important to check for CCJs, understand how long they’re in use, and identify steps to eliminate them. If you have a CCJ, it would be best to deal with it immediately by paying a fee or seeking legal advice to explore your options. Over time, with proper monitoring and reporting, you can improve your credit profile and financial situation.