Loan origination: The process of applying for, evaluating, approving, and issuing a loan is collectively called loan origination. Before disbursing the authorised funds to the borrower, this includes all necessary procedures and practices to confirm if the borrower is qualified, verify terms, assess risk, and the loan terms have been completed.

Loan Origination Process: There are seven essential steps in the loan origination process for anyone who wants to apply for a mortgage or residential loan. It also explains how to apply for a repaid personal loan. This process involves the following seven stages:

- Pre-qualification Stage

- Application Submission

- Application Processing

- Underwriting Stage

- Approval

- Closing Stage

- Servicing

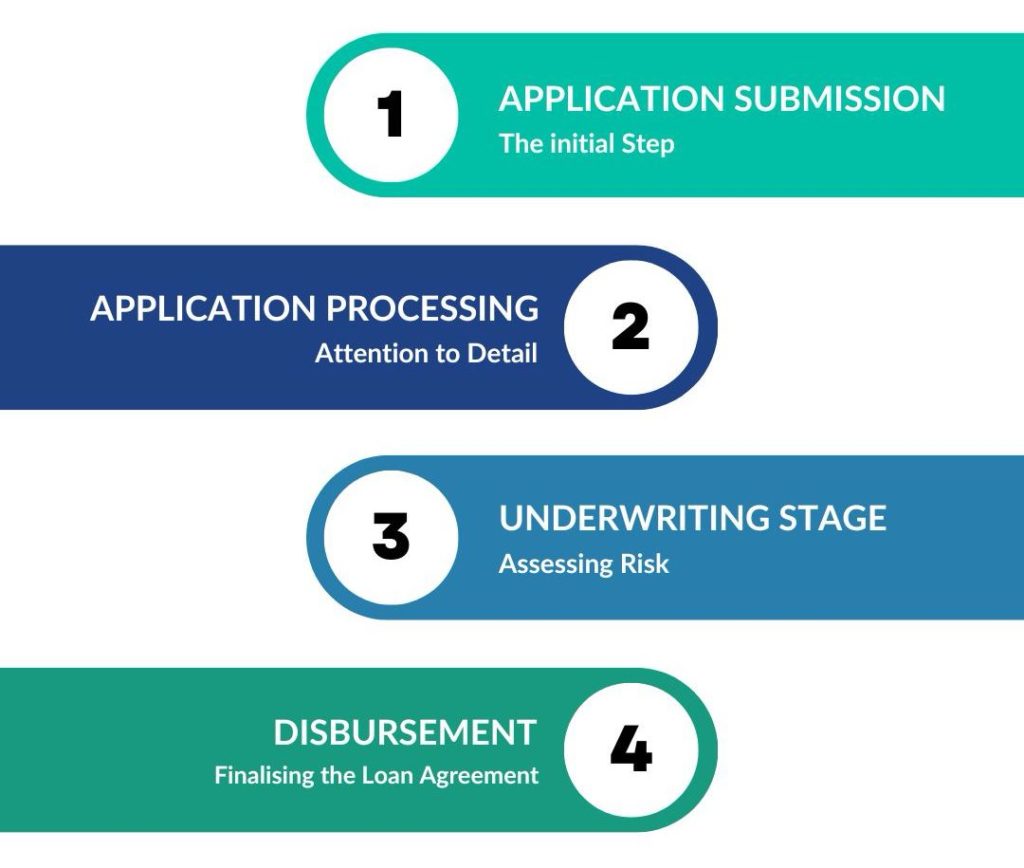

Key Four Stages of the Lending Process

Understanding the credit system in the UK is important for individuals and businesses entering investment opportunities. This journey has four main stages: Application Submission, Application Processing, Underwriting Stage and Disbursement. If people or businesses need to take advantage of potential finance, they want to understand the UK credit trap. Applications must be submitted, processed, registered, and issued under four essential sections of this coverage. The final steps are the closing document, comprehensive inspection, risk assessment, mortgage approval and costs. This knowledge encourages more innovative lending, enables corporate expansion, ensures compliance, and contributes to the balance and prosperity of the UK economy. This is more than just technical documentation.

1. Application Submission: The Initial Step

The first step for purchasers whilst embarking on their loan adventure is to fill out the application form furnished via the lender. With debtors providing many facts about their personal price range, paying extra interest to the element at this point is critical. This information serves as the idea for assessing the borrower’s creditworthiness. Lenders scrutinise every utility, ensuring all data submitted is correct and comprehensive. A thorough danger assessment is part of the underwriting manner, which is essential to this phase. Credit history, earnings statements, assets, liabilities, and different applicable monetary information are just a few of the numerous elements lenders cautiously consider.

For consumers, the first preliminary step in the mortgage journey is filling out a software form furnished with the aid of the lender. Borrowers offer a variety of personal monetary records, so it’s important to pay extra interest to elements at this factor. This data serves as the idea for assessing the creditworthiness of the borrower. Lenders vet every software, confirming that every fact submitted is correct and complete. A thorough threat evaluation is part of the underwriting method, which is crucial to this phase. Credit history, profits statements, belongings, liabilities, and other relevant economic statistics are only some of the numerous elements that creditors cautiously don’t forget.

2. Application Processing: Attention to Detail

Following the submission of the application, it undergoes thorough scrutiny by the credit department. Advanced Loan Origination Systems (LOS) are employed to streamline this process, automating routine checks and flagging incomplete applications. Borrowers may be prompted to provide missing information or clarify details to ensure the accuracy and completeness of the application.

The processing team diligently verifies all aspects of the borrower’s information. This includes meticulously reviewing credit history, financial documents, employment details, and any collateral provided. Before reviewing the software, the goal is to ensure that everyone’s records meet the lender’s criteria and standards.

3. Underwriting Stage: Assessing Risk

The underwriting stage is crucial in the loan approval process. Here, the credit scoring branch monitors applications based on several criteria, such as borrower information and credit rating descriptions. The cause of this analysis is to determine whether or not the mortgage is possible or whether or not changes in expenditure on entertainment or services are necessary to mitigate risks. Underwriters assess economic statements and facts and compare debtors’ capability to pay their mortgages. The use of the present-day era, which includes enterprise rule engines and APIs, streamlines this segment, helping to pick loans based totally on realized value.

4. Disbursement: Finalising the Loan Agreement

After the underwriting section, the software program goes through a final evaluation and transitions into a formal solicitation of funds. Debtors receive targeted mortgage estimates detailing hobby fees, month-to-month payments, and associated charges upon approval. The remaining consists of signing all critical loan documents and settling notable debts. Once this section is complete, the mortgage is formally closed, and the repayment duration evolves, ending the loan origination gadget.

The Significance of Understanding the UK Lending Process

Having access to how credit works within the UK should give people and businesses a sincere leg up on spending wisely It sounds like a wise orientation in dealing with debt and allows businesses to invest as they are needed for the development to execute and do cool things Also, skill rules and games mean that everyone involved feels right about common budgeting, confidence building and balancing want to encourage. What is the end of the story? Debt awareness is not always just knowledge; it is an absolutely powerful force that contributes to the United Kingdom’s economic strength and sustainable growth with the help of customer’s economic choices and resistance to potential risks.

How DataGardener can help you in the Lending Process

DataGardener’s Lending Intelligence solution is a very helpful solution for brokers and lenders within the UK. It dives deeper into the UK market, providing key facts about company age, credit score, turnover, and more, enabling brokers and lenders to uncover new opportunities in today’s fast-paced business environment for those seeking success in the marketplace.

Think Data. Think DataGardener

DataGardener users double their leads and cut research time in half — with smarter data, faster insights, and better decisions.

Conclusion

There are four essential steps in the loan process in the UK: application, processing, underwriting and payment. From submitting loan applications and required documents, this structured process assures thorough investigation and verification, checking factors such as credit history and financial stability. Registration is important in risk assessment and shows how credit can successfully promote responsible lending. The final step is the settlement, which closes the deal and pays the bill. This streamlined process protects the interests of creditors, empowers people and businesses, and encourages smart investment decisions to benefit the UK economy.

Leave a Reply

You must be logged in to post a comment.