What’s in the article ?

- What Do UK Renewable Energy Companies Look Like in 2026?

- Why Do UK Renewable Energy Companies Matter Economically?

- Leading UK Renewable Energy Companies by Sector

- Which UK Clean Energy Sub-Sectors Are Growing Fastest?

- What Policy Mechanisms Are Driving UK Clean Energy Growth?

- Where Are UK Renewable Energy Companies Geographically Concentrated?

- How Does the Procurement Act 2023 Affect UK Clean Energy Suppliers?

- What Structural Constraints Are Slowing UK Renewable Energy Companies?

- What Does the Decade Ahead Hold for UK Renewable Energy Companies?

- Frequently Asked Questions

| What is a UK renewable energy company? A UK renewable energy company is a UK-registered business that generates low-carbon electricity or heat, manufactures or installs clean-energy technology, operates grid, storage or hydrogen infrastructure, or provides services supporting the UK’s legally binding net zero 2050 target. DataGardener’s company dataset tracks these businesses across offshore wind, solar, hydrogen, CCUS, nuclear, heat pumps and associated services — combining Companies House filings, financial health and activity signals that SIC codes alone cannot capture. |

UK renewable energy companies are no longer operating at the edges of the economy. They are at the centre of the UK’s most significant industrial transformation in a generation.

The government has committed over £20 billion to carbon capture alone (HM Treasury). Great British Energy has launched as a publicly backed investment vehicle (gov.uk). The Climate Change Committee has confirmed that clean energy will carry the largest share of the UK’s path to net zero by 2050.

For businesses, investors, and procurement teams, the question is no longer whether this sector matters. It is where the opportunities are concentrated and how to engage with them before others do.

What Do UK Renewable Energy Companies Look Like in 2026?

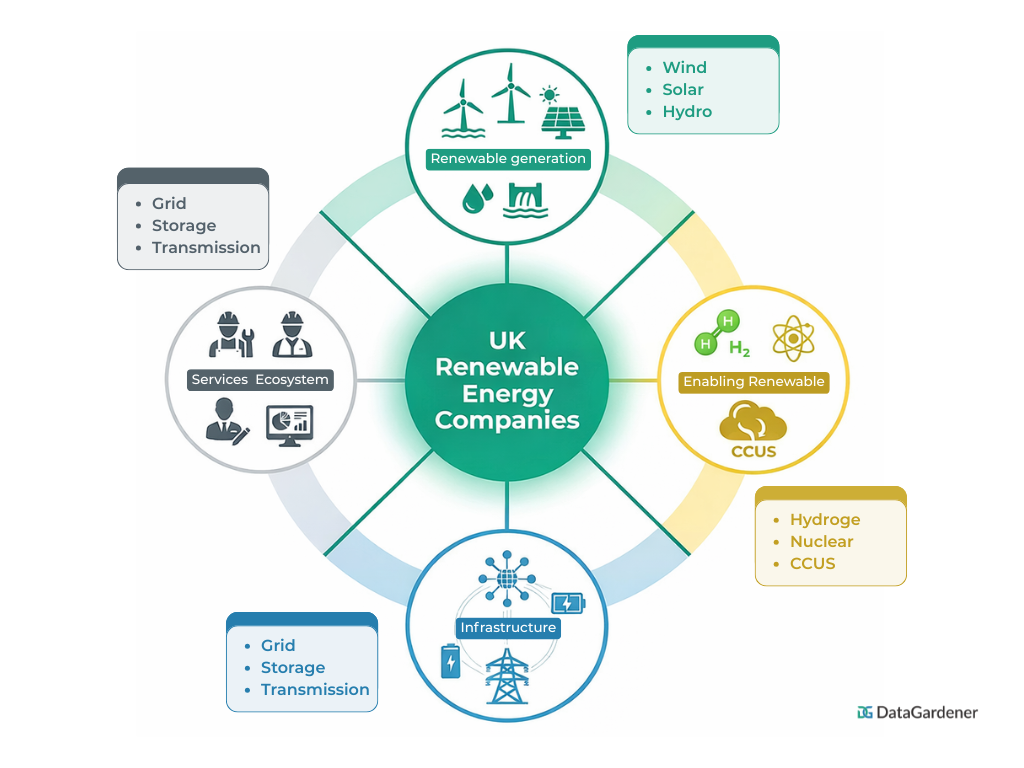

UK renewable energy companies — also referred to as clean energy firms or low-carbon technology companies — now span a far broader range of activities than generation alone.

In 2023, approximately 47 per cent of the UK’s electricity came from renewable sources, according to the Department for Energy Security and Net Zero. Offshore wind contributed over 13 per cent of total generation, placing the UK among global leaders in deployment.

DataGardener’s index of UK company filings identifies thousands of active businesses across renewable generation, low-carbon technology, grid infrastructure, storage and clean-energy services as of Q1 2026, with new-incorporation rates in hydrogen and battery storage growing fastest year-on-year.

The sector today includes renewable generation across wind, solar, and hydro, low-carbon technologies such as nuclear and hydrogen, grid infrastructure, storage, and energy analytics, and a growing services layer of installation, maintenance, and environmental consultancy.

What distinguishes 2026 is the alignment between policy, funding, and market demand driving growth simultaneously from multiple directions.

Why Do UK Renewable Energy Companies Matter Economically?

The clean energy sector is already a material part of the UK economy. Recent estimates place its value at over £70 billion, with approximately 250,000 people employed across renewable energy and supporting industries.

Offshore wind alone is expected to support up to 100,000 jobs by 2030. Furthermore, the sector is driving industrial innovation in hydrogen, nuclear, and grid technology whilst generating high-value employment in engineering, manufacturing, and research and development.

For procurement teams and investors, this translates directly into commercial relevance. UK clean energy firms are no longer a niche or specialist category — they are a central pillar of the UK’s long-term growth strategy.

Organisations that engage early are positioning themselves ahead of a structural shift that will reshape supply chains, procurement requirements, and investment landscapes across the economy.

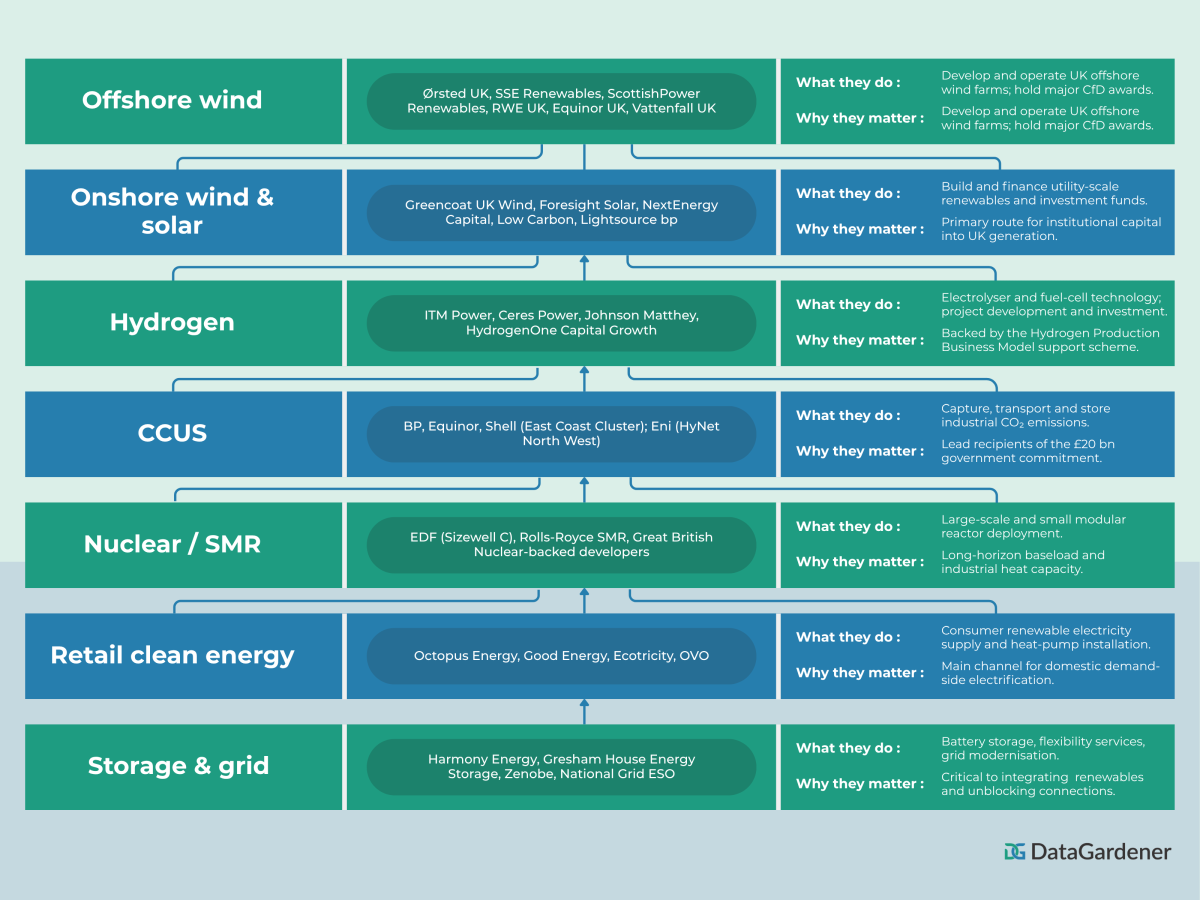

Leading UK Renewable Energy Companies by Sector

The table below summarises representative UK players across the main clean-energy sub-sectors. It is not an exhaustive ranking — entity names, ownership and financial standing change constantly. For a continuously updated, verified list, use DataGardener’s UK renewable energy company database, which indexes Companies House filings, beneficial ownership and sector activity signals in real time.

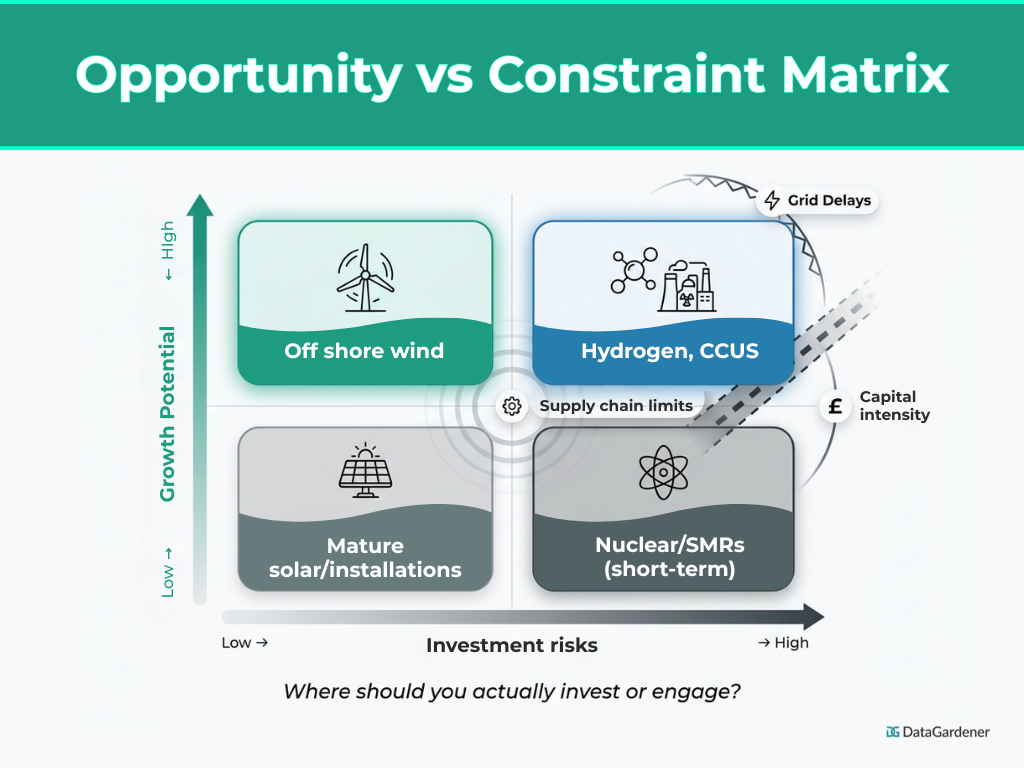

Which UK Clean Energy Sub-Sectors Are Growing Fastest?

The most significant opportunities sit within specific sub-sectors where government backing, private investment, and technological development are converging simultaneously.

Offshore wind

Offshore wind is the most mature frontier sector. The UK holds over 14 gigawatts of installed capacity, the largest in the world, with a government target of 50 gigawatts by 2030. Established supply chains and ongoing expansion make this the lowest-risk entry point for new investors and suppliers.

Carbon Capture, Utilisation and Storage (CCUS)

Carbon Capture, Utilisation, and Storage has received a £20 billion government commitment. The East Coast Cluster and HyNet North West lead the initial deployment phase, forming the backbone of industrial decarbonisation. CCUS is capital-intensive but remains one of the most heavily policy-supported areas of the entire sector.

Hydrogen

Hydrogen is targeted to reach 10 gigawatts of low-carbon production capacity by 2030 under the UK Hydrogen Strategy. The Hydrogen Production Business Model provides revenue support to make early-stage projects commercially viable. Regulatory and funding frameworks are actively reducing investment risk.

Nuclear and Small Modular Reactors

Nuclear and Small Modular Reactors represent the longer-term play. The government is investing in Sizewell C whilst supporting SMR development via Great British Nuclear. SMRs are expected to reduce construction costs and timelines compared to traditional nuclear plants.

Heat pumps and electrification

Heat pumps and electrification are growing rapidly, driven by the Boiler Upgrade Scheme and tightening building regulations. This creates a high-growth installation and services market with relatively low capital requirements.

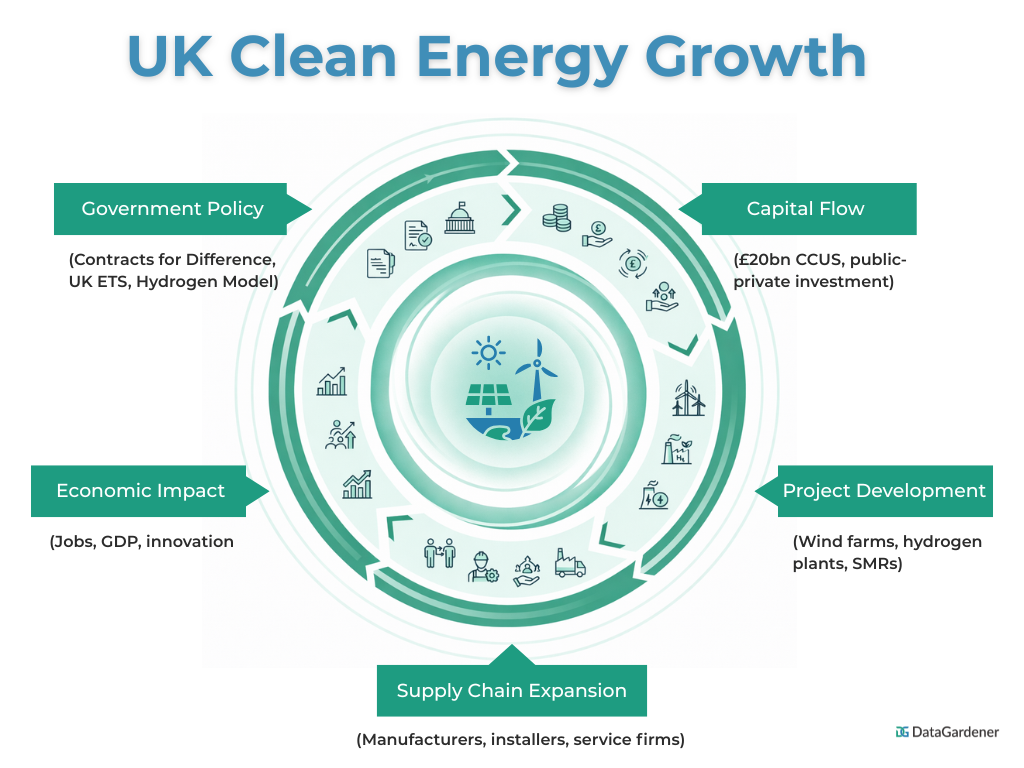

What Policy Mechanisms Are Driving UK Clean Energy Growth?

Understanding the policy landscape is not optional for businesses engaging with this sector. These frameworks directly determine which projects scale and which stall.

Great British Energy provides public investment backing to accelerate deployment. Contracts for Difference (CfD) guarantees price stability for renewable projects, reducing revenue risk for developers. The UK Emissions Trading Scheme applies carbon pricing that shapes industrial behaviour and investment decisions.

The Hydrogen Production Business Model provides revenue certainty to attract private capital to early-stage projects. The Net Zero Innovation Portfolio funds emerging technologies representing the next phase of the transition.

For procurement teams and investors, these mechanisms define the commercial environment — they determine which parts of the UK renewable energy landscape grow fastest and which face structural barriers.

Where Are UK Renewable Energy Companies Geographically Concentrated?

Clean energy growth in the UK is not evenly distributed. It is concentrated in specific regions where infrastructure, policy, and investment are aligned.

The Humber is positioning itself as the UK’s first net-zero industrial cluster, anchored by CCUS and hydrogen activity. Teesside and the North West are home to the East Coast Cluster and HyNet, receiving the bulk of the government CCUS commitment. Scotland dominates UK onshore wind capacity and generates a disproportionate share of total renewable electricity.

Wales is developing hydrogen production capabilities supported by geography and policy. The South West holds emerging potential in tidal and marine energy.

For procurement teams and investors, regional concentration is actionable intelligence. It determines where suppliers, infrastructure investment, and skilled labour are clustering right now.

How Does the Procurement Act 2023 Affect UK Clean Energy Suppliers?

The Procurement Act 2023, in force since 24 February 2025, raises the bar for suppliers bidding on UK public-sector clean energy work.

Procurement teams must now demonstrate greater transparency in supplier selection, stronger social-value weighting, and more rigorous financial and beneficial-ownership verification. For UK renewable energy companies supplying into public-sector contracts, compliance credentials, sustainability disclosures and financial stability are no longer a differentiator — they are a prerequisite.

A practical problem compounds this: SIC codes only partially capture clean-energy activity. Hydrogen, fusion, grid flexibility services and integrated energy offerings fall across multiple classifications or sit outside established codes entirely. Identifying credible clean-energy suppliers therefore requires data infrastructure that looks beyond rigid taxonomies — combining filings, financial signals and activity data.

DataGardener’s UK company database is built for exactly this problem. It continuously indexes Companies House records, financial health indicators, beneficial ownership and sector-specific activity signals, so procurement and investment teams can verify UK renewable energy suppliers in minutes rather than weeks — including the hydrogen, CCUS and energy-services firms that SIC-based searches miss.

What Structural Constraints Are Slowing UK Renewable Energy Companies?

The challenges facing the sector are specific and structural rather than generic.

Grid connection delays are currently among the most significant constraints. Some projects face waiting periods of up to fifteen years for network access, directly limiting deployment pace. Planning and permitting timelines, particularly for onshore wind, have historically been restrictive, though recent policy changes are beginning to ease them.

Supply chain bottlenecks in offshore wind components, including turbine foundations and specialist installation vessels, are limiting growth relative to government targets. Additionally, high upfront capital requirements remain a barrier for infrastructure-heavy projects without long-term revenue certainty.

These constraints determine not just which sectors are growing but which projects within those sectors actually get built.

What Does the Decade Ahead Hold for UK Renewable Energy Companies?

By 2030, offshore wind capacity is targeted at 50 gigawatts, hydrogen production at 10 gigawatts, and CCUS clusters are expected to be operational. SMRs are likely to move through planning and into early deployment.

All of this feeds into the legally binding net-zero 2050 commitment that frames every major clean energy investment decision in the UK.

UK renewable energy companies are not a short-term trend. They represent a long-term restructuring of the economy. The businesses, investors, and procurement teams that engage with this sector now are the ones most likely to benefit from the scale of change already underway.

The opportunity is not approaching. It is already here.

Explore the UK Renewable Energy Company Database →

DataGardener gives procurement, investment and ESG teams a verified, real-time view of UK clean-energy suppliers:

- Filter by sector — offshore wind, onshore wind, solar, hydrogen, CCUS, SMR, heat pumps, grid and storage

- Verify financial health, directorship history and beneficial ownership

- Track new incorporations, M&A activity and funding events

- Export clean data for due diligence, tendering and CRM enrichment

Start your search on datagardener.com →