UK business formation in 2025 tells a story that goes far deeper than headlines suggest. Businesses do not just appear out of nowhere. They form in response to what is happening around them. Sometimes opportunity pulls them forward. Sometimes pressure forces them into existence. In 2025, the UK delivered plenty of both.

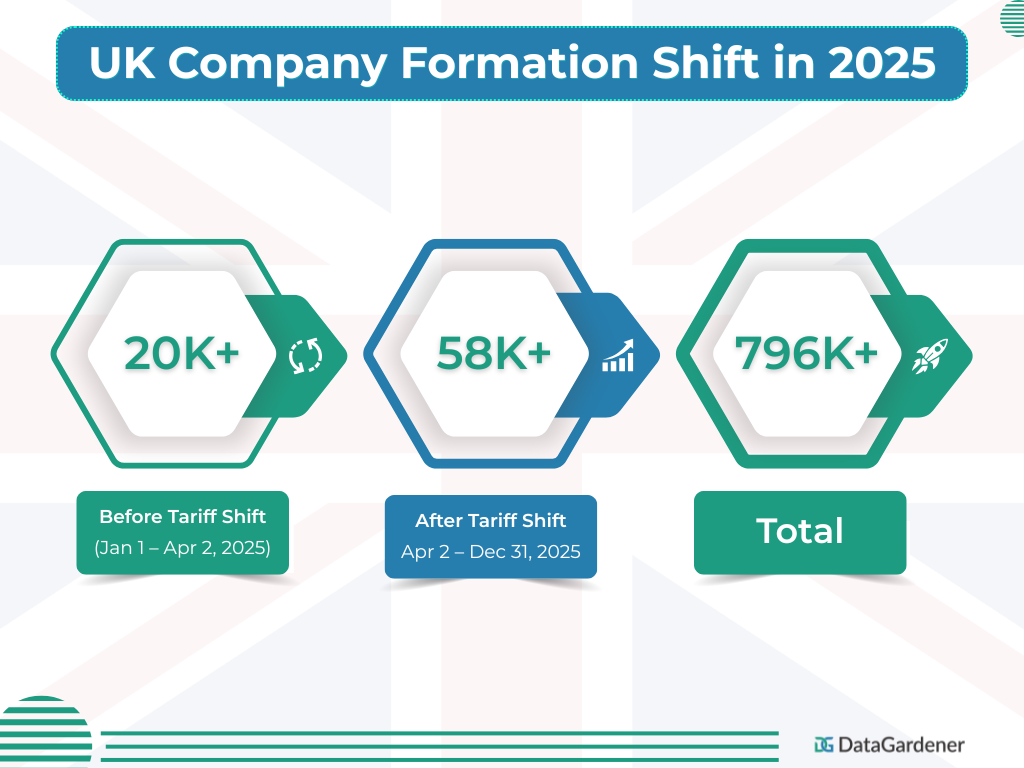

In total, 796,889 new companies were registered. However, that number becomes far more revealing when split by timing. According to Companies House, 207,669 companies formed between 1 January and 2 April. A further 589,708 followed between 2 April and 31 December. That shift shows exactly how sharply founder behaviour changed once external conditions moved.

What Does UK Business Formation Data Actually Tell Us?

The totals catch attention. But totals only tell you so much.

What matters is what sits underneath. UK business formation is no longer spreading evenly across the economy. It is concentrating in specific places, where momentum already exists.

You can see it clearly in where activity is clustering:

- Artificial intelligence and data-led services

- Green energy and sustainability-driven models

- Health tech and biotech

- Digital commerce ecosystems

- Financial technology embedded into everyday transactions

This is not trend chasing. It is alignment. Founders are not asking what can be built. They are asking what needs to be built next. Furthermore, the answer is consistently pointing toward sectors where demand and regulatory momentum are converging at the same time.

How Has the Profile of New UK Companies Changed?

If you still imagine growth as slow expansion and steady hiring, that model is already outdated.

The businesses forming through UK business formation activity now are lighter, faster, and far less predictable than previous generations of startups. They operate in tight cycles. They adapt quickly. They scale through networks rather than physical infrastructure. Instead of spreading wide, they go deep into one niche early.

On paper, they often look small. However, once they start moving, they behave very differently from what traditional evaluation frameworks are designed to assess.

Most evaluation models were built for stability. These businesses are built for movement. As a result, they are harder to read using conventional financial signals alone.

Which UK Sectors Are Seeing the Strongest Business Formation Growth?

Not every sector described as emerging actually earns that label. Some attract attention. Far fewer convert that attention into sustainable revenue.

The difference comes down to one thing: alignment. The sectors pulling ahead sit precisely where demand meets structural inevitability.

- AI businesses that remove cost or unlock processing speed

- Fintech solutions that integrate into existing systems rather than replacing them

- Green energy models that move with regulatory momentum rather than against it

These sectors are not just growing. They are being pulled forward by forces larger than any individual business within them. Consequently, revenue is showing up earlier than market cycles would traditionally predict.

Are Established UK Companies Also Driving Business Formation Trends?

It is not only startups contributing to UK business formation activity. Established companies are moving in as well, and not cautiously.

They are redirecting strategic focus toward sustainability capabilities, data infrastructure, and platform-led commercial models. This is not experimentation. It is a direct response to where commercial value is clearly moving.

That shift changes the competitive dynamic entirely. It is no longer a contest between new and old. Instead, it has become a contest between speed and scale.

How Are UK Trade Agreements Influencing New Business Formation?

UK business formation does not evolve in isolation from global trade conditions. In fact, trade agreements are actively reshaping which sectors attract new company activity and where new demand corridors are opening.

The India–UK Comprehensive Economic and Trade Agreement is a significant example. With tariffs reduced on 90 per cent of UK exports and 99 per cent of Indian goods, entire sectors are opening new commercial pathways. Its April 2026 rollout is likely to accelerate cross-border services, fintech integration, and talent mobility between the two economies.

Additionally, the UK is building parallel momentum through several other frameworks. The CPTPP integration is opening access to Asia Pacific markets. The UK–South Korea Digital Trade Agreement is advancing AI and digital standards. The Economic Prosperity Deal with the United States is strengthening supply chain collaboration and green technology investment.

All of this feeds directly back into new company formation. Businesses do not just respond to current markets. They respond to where markets are about to expand.

Why Does Timing Matter So Much in UK Business Formation Analysis?

UK business formation tells you where companies are going. External forces decide how far they get. The 2025 timing split makes that relationship explicit.

Companies formed before April behaved differently from those formed after. Earlier formations leaned into global exposure. Later formations show more caution, stronger localisation, and a clearer orientation toward services over product-heavy models.

Moreover, the impact shows up quickly. Younger businesses, particularly those tied to import-heavy models, react faster to external shocks. Revenue volatility hits them earlier and harder than established counterparts.

Therefore, timing is no longer a background detail in formation analysis. It is a defining variable that changes what the data actually means.

What Does UK Business Formation Data Reveal That Headlines Miss?

The real intelligence in UK business formation data is not found in totals. It lives in patterns.

Which sectors are forming fastest. Which are dissolving at above-average rates. How post-tariff timing has shifted founder behaviour. Where trade agreement corridors are creating demand before it becomes visible to the broader market.

According to the Office for National Statistics, business demography data at sector and regional level provides a further layer of intelligence that aggregate formation counts cannot capture alone.

This distinction separates a count from genuine intelligence. One tells you how many. The other tells you why, where, and what comes next.

At DataGardener, we track UK company formation data across 35 plus integrated sources. Consequently, lenders, investors, and analysts can access the signals that matter before they become obvious to the wider market.

Want to explore UK business formation trends for your sector? Talk to the DataGardener team.